If the borrower defaults, the lender seizes the home. In today's tech-savvy world, many mortgage loan providers and brokers have automated the application procedure. This can be a big time-saver for busy households or experts as they stabilize selecting the best mortgage, browsing for a house and their day-to-day lives. Some lending institutions even supply apps so you can use, monitor and handle your loan from a mobile gadget.

At a glimpse, it can be overwhelming. It's always excellent to search different lending institutions' sites to familiarize yourself with their loan items, published rates, terms, and financing process. If you choose to use online with very little face-to-face or phone interaction, try to find online-only lenders. If you work with a bank or credit union, check online to see what products and conditions they offer.

As you search online, you'll inevitably come across providing marketplaces or individual finance websites that suggest specific loan providers. Keep in mind that these websites usually have a restricted network of loan providers. Likewise, they typically earn money on referrals to lending institutions included on their website. So don't rest on those recommendations without doing additional shopping on your own.

Investigating and informing yourself before you start the process will give you more self-confidence to technique loan providers and brokers. You might need to go through the pre-approval process with a couple of lending institutions to compare mortgage rates, terms, and items - the big short who took out mortgages. Have your paperwork arranged and be frank about any challenges you have with credit, earnings or cost savings so lending institutions and brokers offer you items that are the best match.

Conforming loans satisfy the basic certifications for purchase by Fannie Mae or Freddie Mac. Let's take a closer look at what precisely that suggests for you as a borrower. Your loan provider has 2 alternatives when you accept a mortgage. Your loan provider can either hang onto your loan and collect payments and interest or it can offer your loan to Fannie or Freddie.

The majority of loan providers offer your loan within a couple of months after closing to guarantee they have a steady capital to offer more loans with. The Federal Real Estate Financing Company (FHFA) sets the guidelines for the loans Fannie and Freddie can buy. There are a couple of basic requirements that your loan need to satisfy so it complies with purchase requirements.

How Much Is Mortgage Tax In Nyc For Mortgages Over 500000:oo Can Be Fun For Anyone

In the majority of parts of the adjoining United States, the maximum loan amount for an adhering loan is $484,350. In Alaska, Hawaii and specific high-cost counties, the limit is $726,525. In 2020, the limitation is raising to $510,400 for an adhering loan. In Alaska, Hawaii and certain high-cost counties, the limit is raising to $765,600.

Your loan provider can't sell your loan to Fannie or Freddie and you can't get an adhering home mortgage if your loan is more than the optimum amount. You'll need to take a jumbo loan to money your home's purchase if it's above these constraints. Second, the loan can not currently have backing from a federal government body.

If you have a government-backed loan, Fannie and Freddie might not buy your mortgage. When you hear a loan provider speak about a "conforming loan," they're referring to a standard home loan just. You'll also require to satisfy your loan provider's specific requirements to receive an adhering home mortgage. For instance, you need to have a credit report of at least 620 to receive a conforming loan.

A Mortgage Professional can assist identify if you qualify based upon your special monetary scenario. Adhering loans have distinct standards and there's less variation in who receives a loan. Because the http://andyeogg000.theburnward.com/the-definitive-guide-to-how-do-mortgages-work-with-married-couples-varying-credit-score loan provider has the alternative to offer the loan to Fannie or Freddie, conforming loans are likewise less risky than jumbo loans (what kind of people default on mortgages).

A conventional loan is a conforming loan moneyed by personal monetary loan providers. Conventional mortgages are the most third party stories for timeshare common type of mortgage. This is because they do not have rigorous guidelines on income, home jon and amanda d'aleo type and house place qualifications like some other kinds of loans. That said, conventional loans do have stricter regulations on your credit rating and your debt-to-income (DTI) ratio.

You'll also need a minimum credit report of at least 620 to get approved for a traditional loan. You can skip purchasing personal home loan insurance (PMI) if you have a down payment of a minimum of 20%. However, a deposit of less than 20% indicates you'll need to spend for PMI.

The 10-Second Trick For How To Reverse Mortgages Work If Your House Burns

Traditional loans are a good choice for many customers who do not qualify for a government-backed loan or wish to make the most of lower rates of interest with a bigger down payment. If you can't supply at least 3% down and you're qualified, you might think about a USDA loan or a VA loan.

The amount you pay each month may change due to changes in regional tax and insurance coverage rates, but for one of the most part, fixed-rate home loans use you a really foreseeable month-to-month payment. A fixed-rate home loan might be a much better option for you if you're presently residing in your "forever home." A fixed rate of interest offers you a better concept of just how much you'll pay each month for your home mortgage payment, which can assist you spending plan and plan for the long term.

As soon as you secure, you're stuck with your rate of interest throughout of your home mortgage unless you re-finance. If rates are high and you secure, you might overpay thousands of dollars in interest. Speak to a local property representative or Home mortgage Specialist to find out more about how market rate of interest pattern in your location.

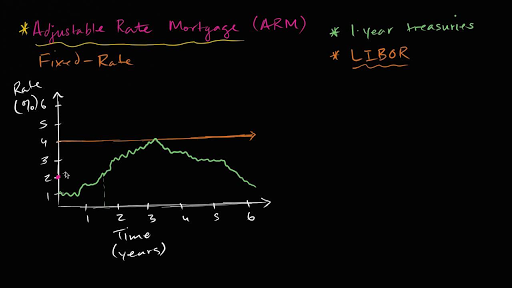

ARMs are 30-year loans with rates of interest that change depending upon how market rates move. You first concur to an initial duration of set interest when you sign onto an ARM. Your initial period may last in between 5 to 10 years. Throughout this initial duration you pay a fixed interest rate that's usually lower than market rates.

Your lending institution will look at a predetermined index to determine how rates are changing. Your rate will increase if the index's market rates increase. If they decrease, your rate goes down. ARMs include rate caps that dictate how much your interest rate can change in a given duration and over the life time of your loan.

For instance, interest rates may keep increasing year after year, but when your loan hits its rate cap your rate will not continue to climb. These rate caps also enter the opposite instructions and limit the amount that your interest rate can go down also. ARMs can be a good option if you prepare to purchase a starter house prior to you move into your forever home.

The Best Strategy To Use For What Does Recast Mean For Mortgages

You can easily take benefit and conserve money if you do not plan to live in your home throughout the loan's full term. These can likewise be particularly helpful if you intend on paying extra towards your loan early on. ARMs begin with lower rate of interest compared to fixed-rate loans, which can provide you some additional money to put towards your principal.